Beta launch of the first ESRS Reporting Software

July 12, 2023

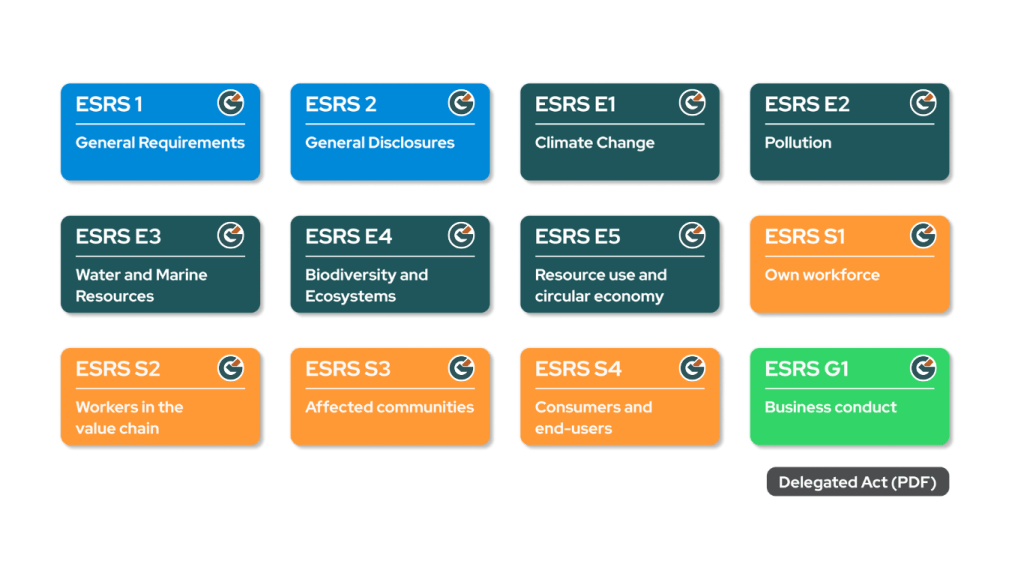

July 31, 2023. The Commission has adopted the European Sustainability Reporting Standards (ESRS), supplementing Directive 2013/34/EU of the European Parliament and of the Council as regards sustainability reporting standards, for use by all companies subject to the Corporate Sustainability Reporting Directive (CSRD).

This delegated act is based on Article 29b(1), first subparagraph, of the Accounting Directive. It specifies the European Sustainability Reporting Standards (ESRS) undertakings shall use to carry out their sustainability reporting in accordance with Articles 19a and 29a of the Accounting Directive.

The delegated act includes 12 standards:

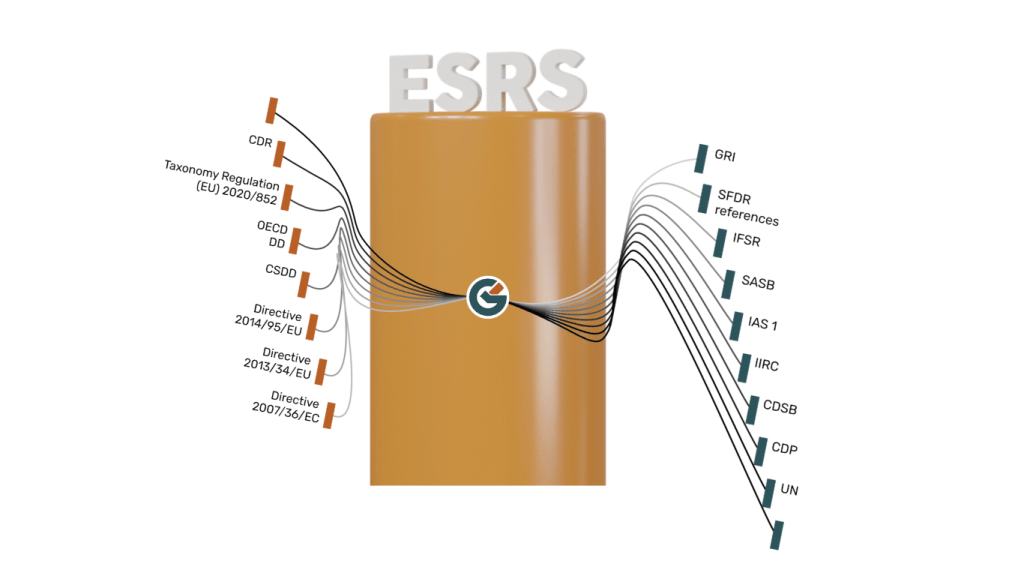

September 4th, 2023, EFRAG and GRI published a joint statement on the high level of interoperability achieved between the European Sustainability Reporting Standards (ESRS) and the GRI Standards.

Following the requirement of the CSRD to adopt a double materiality approach and to take account of existing standards, ESRS and GRI definitions, concepts and disclosures regarding impacts are fully or, when full alignment was not possible due to the content of the CSRD mandate, closely aligned.

Existing GRI reporters will be well prepared to report under the ESRS. Entities reporting under ESRS are considered as reporting with reference to the GRI Standards and will therefore avoid the burden of multiple reporting.

August 23rd, 2023, EFRAG published the paper “Interoperability between ESRS and ISSB standards EFRAG assessment at this stage and mapping table “.

The objective of this paper is to present the EFRAG’s assessment at this stage on the interoperability between ESRS 2 General Disclosures and ESRS E1 Climate and IFRS S1 & S2 Climate-related Disclosures and to provide a supporting mapping table. This paper and the climate-related disclosures mapping table is a contribution to the ongoing joint work with the ISSB on interoperability guidance on ESRS and ISSB standards.

Background: The CSRD requires that in adopting the Delegated Acts the European Commission shall to the greatest extent possible take account of the work of global standard-setting initiatives. In addition, ESRS should contribute to convergence of global standards to reduce the risk of inconsistent reporting requirements for undertakings that operate globally.

EFRAG stated that It is important to present the EFRAG’s assessment at this stage on the interoperability between ESRS 2 General Disclosures and ESRS E1 Climate and IFRS S1 & S2 Climate-related Disclosures and to provide a supporting mapping table, which is a contribution to the ongoing joint work with the ISSB on interoperability guidance on ESRS and ISSB standards.

Generation Impact Global follows EFRAG, GRI, IFRS statements and presents interoperability between frameworks in the system for easy reporting sustainability and avoid company burden.