ESG Reporting readiness assessment

Sustainability reporting requirements are expanding rapidly. Regulations such as the Corporate Sustainability Reporting Directive (CSRD), the Sustainable Finance Disclosure Regulation (SFDR), and international standards from the ISSB/IFRS and GRI now affect thousands of organisations worldwide. For many ESG, compliance, and sustainability teams, the first question is simple but critical: which frameworks actually apply to us, and how ready are we?

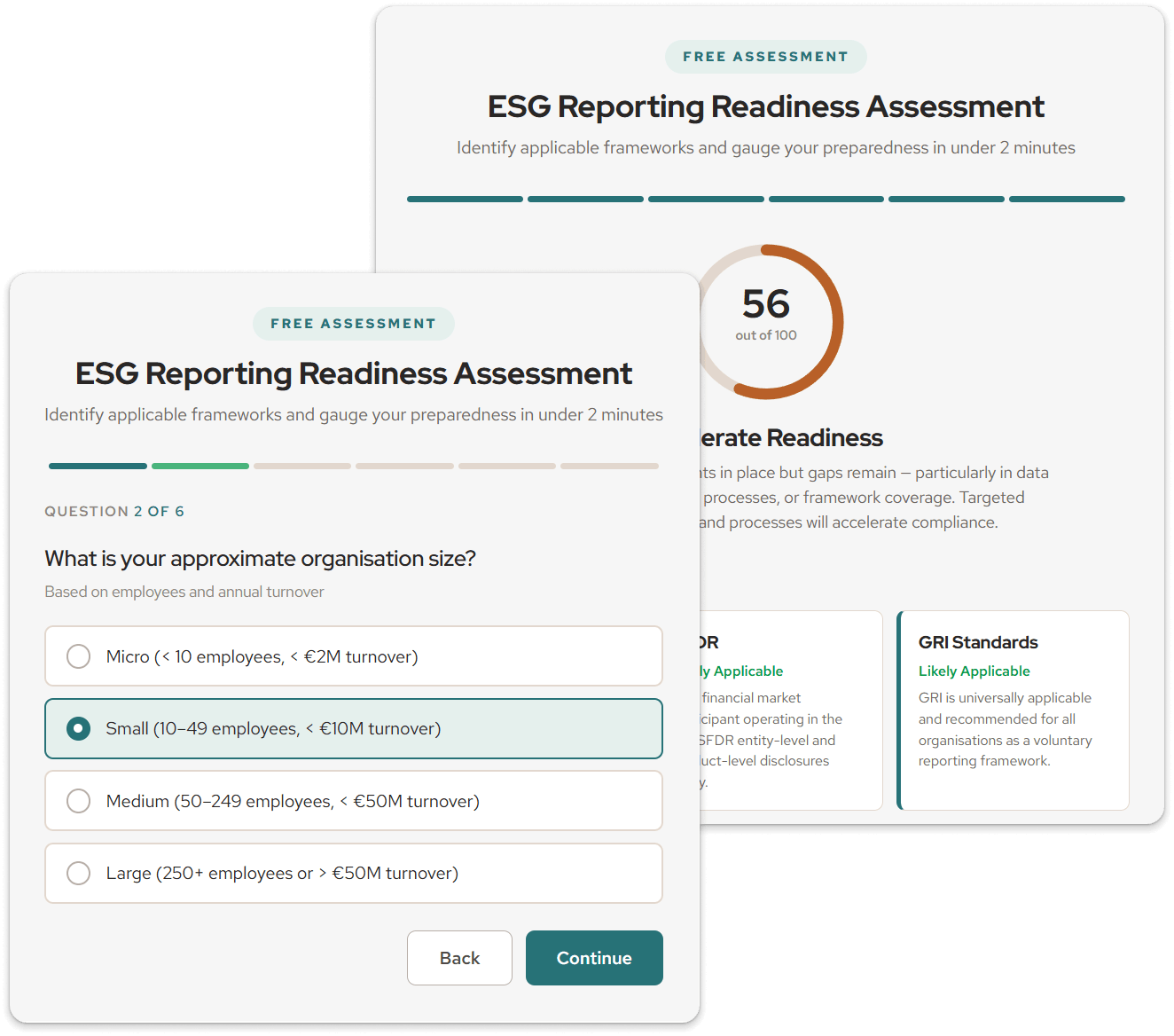

To help answer that question, we have built a free ESG Reporting Readiness Assessment. This interactive tool evaluates your organisation’s profile against the major sustainability reporting frameworks and produces a readiness score with personalised recommendations. It covers CSRD/ESRS, SFDR, GRI, IFRS Sustainability Disclosure Standards (ISSB), and the UN Sustainable Development Goals (SDGs) — the five frameworks that define the current ESG reporting landscape.

Go to tool

What does ESG mean and why does reporting readiness matter?

ESG stands for Environmental, Social, and Governance — the three pillars used to evaluate an organisation’s sustainability performance and risk profile. ESG reporting translates these pillars into structured disclosures that investors, regulators, and stakeholders use to assess non-financial performance. For businesses, understanding what ESG means in practice has moved from a reputational exercise to a regulatory obligation.

The reporting landscape is now defined by several overlapping frameworks, each with distinct scope, audience, and requirements. Getting clarity on which frameworks apply — and how ready your systems are to produce compliant data — is the essential first step. At Generation Impact Global, our ESG data management platform helps organisations operationalise this process across multiple frameworks simultaneously.

The Six Frameworks covered

CSRD / ESRS

The Corporate Sustainability Reporting Directive requires in-scope EU companies and certain non-EU companies to report against the European Sustainability Reporting Standards (ESRS). It applies based on company size, listing status, and turnover thresholds. CSRD represents the most comprehensive mandatory ESG reporting regime globally, requiring double materiality assessments and third-party assurance.

SFDR

The Sustainable Finance Disclosure Regulation targets financial market participants — asset managers, pension funds, and investment advisers — operating in the EU. It classifies financial products under Articles 6, 8, or 9 based on their sustainability characteristics and requires entity-level and product-level disclosures, including principal adverse impact (PAI) indicators.

GRI Standards

The Global Reporting Initiative (GRI) standards are the world’s most widely adopted voluntary sustainability reporting framework. GRI is sector-agnostic and stakeholder-oriented, making it suitable for organisations of all sizes and geographies. GRI reporting is also referenced as a basis for CSRD/ESRS compliance.

IFRS / ISSB Sustainability Standards

The IFRS Sustainability Disclosure Standards (S1 and S2) issued by the International Sustainability Standards Board provide a global baseline for investor-focused sustainability reporting. Jurisdictions including the UK, Australia, Japan, and others are adopting or considering ISSB-aligned requirements. These standards are designed to complement financial reporting under IFRS Accounting Standards.

UN SDGs

The 17 UN Sustainable Development Goals provide a universal framework for aligning business activities with global sustainability targets. While SDG reporting is voluntary, it is increasingly expected by investors and integrated into ESG ratings. Our SDG Mapper tool helps organisations map their disclosures to specific SDG targets.

EU Taxonomy

The EU Taxonomy is a classification system defining environmentally sustainable economic activities. It applies to organisations subject to CSRD and to financial market participants under SFDR, requiring disclosure of Taxonomy-aligned revenue, CapEx, and OpEx.

| Framework | Type | Primary Audience | Geography |

|---|---|---|---|

| CSRD / ESRS | Mandatory | Broad stakeholders | EU + non-EU (thresholds) |

| SFDR | Mandatory | Investors / financial products | EU |

| GRI | Voluntary (referenced in CSRD) | All stakeholders | Global |

| IFRS / ISSB | Mandatory (jurisdiction-dependent) | Investors | Global (adopting jurisdictions) |

| SDGs | Voluntary | All stakeholders | Global |

| EU Taxonomy | Mandatory (linked to CSRD/SFDR) | Investors + regulators | EU |

What does ESG mean in business?

In a business context, ESG refers to the integration of environmental, social, and governance considerations into corporate strategy, risk management, and reporting. Environmental factors include carbon emissions, energy efficiency, resource consumption, and biodiversity impact. Social factors encompass labour practices, diversity and inclusion, supply chain standards, and community engagement. Governance covers board composition, executive compensation, anti-corruption policies, and transparency.

For financial institutions and investors, ESG analysis has become a core part of due diligence. ESG investing — the practice of incorporating these factors into investment decisions — now accounts for a significant share of global assets under management. ESG funds apply specific screening criteria or thematic strategies to align portfolios with sustainability outcomes. Understanding ESG meaning in business is therefore not just about reporting — it shapes how capital is allocated, how risk is priced, and how companies compete for investment.

Identify applicable frameworks and gauge your preparedness in under 2 minutes

Note: This assessment is indicative and educational. It does not constitute legal, compliance, or financial advice. Framework applicability depends on additional factors not captured here. For detailed fiscal impact modelling of decarbonisation scenarios, see the OECD EDISON tool, which provides a structured framework for evaluating fiscal consequences of climate transition at national level. For authoritative regulatory guidance, consult the relevant legislative texts directly.

Get notified when new tools launch

SubscribeHow ESG scores and ratings connect to reporting

ESG scores and ESG ratings are assessments produced by third-party agencies — such as MSCI, Sustainalytics, or Moody’s — based on an organisation’s disclosed and publicly available ESG data. The quality and completeness of your reporting directly influences your ESG score. Organisations with structured, framework-aligned reporting processes consistently achieve higher ESG ratings, which in turn affect cost of capital, investor confidence, and inclusion in ESG funds and sustainable investment products.

An ESG report is the primary vehicle for communicating this data. Whether produced under GRI, ESRS, or ISSB standards, the report aggregates quantitative metrics and qualitative disclosures into a format that stakeholders can assess. Understanding what an ESG report contains — and how the data feeds into external ratings — helps teams prioritise their data collection efforts and identify the most impactful areas for improvement.

Understanding what ESG scores mean and how they are derived is essential for any team responsible for sustainability reporting. The readiness assessment above helps identify gaps that, if addressed, can improve both regulatory compliance and external ESG evaluations.

IFRS vs GAAP: where ISSB Fits

A common question for multinational organisations is how IFRS Sustainability Disclosure Standards relate to existing financial reporting frameworks. The definition of IFRS — International Financial Reporting Standards — encompasses a set of accounting standards issued by the IASB that govern how financial transactions and events are reported. IFRS is used in over 140 jurisdictions worldwide, while US GAAP (Generally Accepted Accounting Principles) is the primary standard in the United States.

The key differences between IFRS and GAAP span revenue recognition, lease accounting, inventory valuation, and the treatment of intangible assets. In the sustainability reporting context, the ISSB standards (S1 and S2) are built on IFRS conceptual foundations — but jurisdictions using GAAP may adopt equivalent requirements through the SEC’s climate disclosure rules or voluntary adoption. Understanding the meaning of IFRS and how it intersects with sustainability standards is increasingly important for finance teams managing both financial and non-financial disclosures.

For organisations reporting under both IFRS Accounting Standards and IFRS Sustainability Standards, the interoperability features of the Generation Impact platform ensure consistent data treatment across financial and non-financial disclosures.

Moving from assessment to action

The readiness assessment above is a starting point. Organisations looking to operationalise their ESG reporting should consider building structured data collection workflows, implementing questionnaire-based ESG data gathering, and establishing KPI calculation logic that maps to multiple frameworks simultaneously. The Generation Impact Global platform supports this end-to-end, from data collection through to regulatory-ready outputs for CSRD, SFDR, GRI, TCFD/ISSB, and SDG reporting.

Frequently Asked Questions

What does ESG stand for?

ESG stands for Environmental, Social, and Governance. These three pillars are used by investors, regulators, and stakeholders to evaluate an organisation’s sustainability performance and non-financial risk profile.

What is CSRD and who does it apply to?

The Corporate Sustainability Reporting Directive (CSRD) is an EU regulation requiring large companies, listed SMEs, and certain non-EU companies to report sustainability data under the European Sustainability Reporting Standards (ESRS). It applies based on employee count, turnover, and balance sheet thresholds.

What is the difference between IFRS and GAAP?

IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles, primarily US GAAP) are the two major financial reporting frameworks. Key differences include approaches to revenue recognition, inventory accounting, and lease treatment. The ISSB Sustainability Standards (S1 and S2) are built on IFRS foundations but are designed to be adoptable by jurisdictions using either framework.

What is GRI reporting?

GRI (Global Reporting Initiative) reporting is a voluntary sustainability reporting framework used by organisations worldwide to disclose their environmental, social, and governance impacts. GRI Standards provide a structured approach to stakeholder-oriented sustainability reporting and are referenced within the EU’s CSRD as a basis for compliance.

What is an ESG score and how is it calculated?

An ESG score is a numerical rating assigned by third-party agencies based on an organisation’s sustainability disclosures, policies, and performance. It is calculated using proprietary methodologies that weigh environmental, social, and governance factors. Better reporting quality and framework alignment typically improve ESG scores.

How many SDG goals are there?

There are 17 UN Sustainable Development Goals (SDGs), underpinned by 169 targets. They cover a wide range of global priorities including poverty, climate action, clean energy, responsible consumption, and institutional governance. Organisations increasingly map their ESG disclosures to relevant SDG targets.