The Trustees of the IFRS Foundation announced the formation of the International Sustainability Standards Board (ISSB) on 3 November 2021 at COP26 in Glasgow, following strong market demand for its establishment. The ISSB is developing—in the public interest—standards that will result in a high-quality, comprehensive global baseline of sustainability disclosures focused on the needs of investors and the financial markets.

The ISSB has international support with its work to develop sustainability disclosure standards backed by the G7, the G20, the International Organization of Securities Commissions (IOSCO), the Financial Stability Board, African Finance Ministers and Finance Ministers and Central Bank Governors from more than 40 jurisdictions.

The ISSB has set out four key objectives:

The ISSB builds on the work of market-led investor-focused reporting initiatives, including the Climate Disclosure Standards Board (CDSB), the Task Force for Climate-related Financial Disclosures (TCFD), the Value Reporting Foundation’s Integrated Reporting Framework and industry-based SASB Standards, as well as the World Economic Forum’s Stakeholder Capitalism Metrics.

The ISSB is committed to delivering standards that are cost-effective, decision-useful and market informed.

FRS S1 is effective for annual reporting periods beginning on or after 1 January 2024 with earlier application permitted as long as IFRS S2 Climate-related Disclosures is also applied.

The objective of IFRS S1 is to require an entity to disclose information about its sustainability-related risks and opportunities that is useful to users of general purpose financial reports in making decisions relating to providing resources to the entity.

IFRS S1 requires an entity to disclose information about all sustainability-related risks and opportunities that could reasonably be expected to affect the entity’s cash flows, its access to finance or cost of capital over the short, medium or long term (collectively referred to as ‘sustainability-related risks and opportunities that could reasonably be expected to affect the entity’s prospects’).

IFRS S1 prescribes how an entity prepares and reports its sustainability-related financial disclosures. It sets out general requirements for the content and presentation of those disclosures so that the information disclosed is useful to users in making decisions relating to providing resources to the entity.

IFRS S1 sets out the requirements for disclosing information about an entity’s sustainability-related risks and opportunities. In particular, an entity is required to provide disclosures about:

In-depth explainer of IFRS S1:

IFRS S2 is effective for annual reporting periods beginning on or after 1 January 2024 with earlier application permitted as long as IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information is also applied.

The objective of IFRS S2 is to require an entity to disclose information about its climate-related risks and opportunities that is useful to users of general purpose financial reports in making decisions relating to providing resources to the entity.

IFRS S2 requires an entity to disclose information about climate-related risks and opportunities that could reasonably be expected to affect the entity’s cash flows, its access to finance or cost of capital over the short, medium or long term (collectively referred to as ‘climate-related risks and opportunities that could reasonably be expected to affect the entity’s prospects’).

IFRS S2 applies to:

IFRS S2 sets out the requirements for disclosing information about an entity’s climate-related risks and opportunities. In particular, IFRS S2 requires an entity to disclose information that enables users of general purpose financial reports to understand:

In-depth explainer of IFRS S2:

In March 2022, GRI and the IFRS Foundation signed a Memorandum of Understanding (MoU) to coordinate their work programs and standard-setting activities as well as join each other’s consultative bodies related to sustainability reporting. By working together, the IFRS Foundation and GRI provide two pillars of international sustainability reporting – a first pillar representing investor-focused capital market standards of IFRS Sustainability Disclosure Standards developed by the International Sustainability Standards Board (ISSB), and a second pillar of GRI sustainability reporting requirements set by the Global Standards Setting Board (GSSB), compatible with the first and designed to meet multi-stakeholder needs.

In 2021, GRI responded on the updated strategic direction of the IFRS Foundation and the establishment of a working group. In November 2021, GRI welcomed the announcement of the launch of the ISSB, which included the consolidation of the Climate Disclosure Standards Board (CDSB) and the Value Reporting Foundation (which includes the IIRC and SASB) into the ISSB. GRI has previously had long-running collaborations with both the IIRC and SASB, including a 2021 joint report on how to use GRI and SASB standards together.

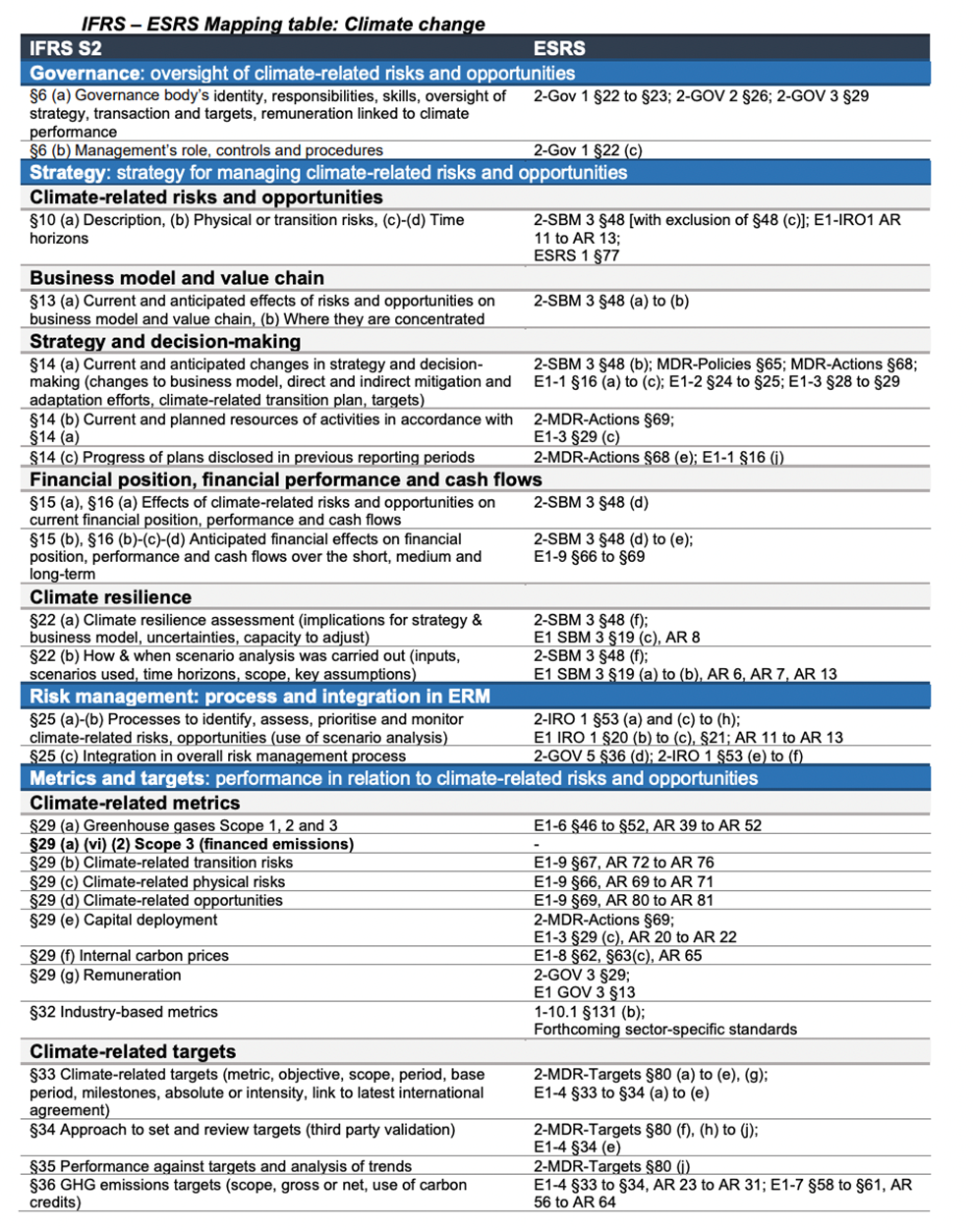

On July 31, 2023 European Commission, EFRAG and ISSB confirm high degree of climate -disclosure alignment.

The European Commission, EFRAG and the ISSB have worked jointly to improve the interoperability of their respective climate-related disclosure requirements in the overlapping climate disclosure standards. This work has successfully led to a very high degree of alignment, reduced complexity and duplication for entities wishing to apply both the ISSB Standards and ESRS.

ESRS and ISSB Standards have been developed within their respective mandates, with some differences on impact materiality beyond an investor’s perspective and coverage of the range of ESG matters in separate standards. However, the work undertaken on interoperability enables an entity to efficiently apply both sets of climate-related standards with minimized duplication of effort.

The mapping table below, published by EFRAG August 23, 2023, illustrates the high level of interoperability achieved and can assist preparers and users in identifying the ESRS information corresponding to IFRS S1 & S2 requirements in relation to climate.